{kind=link}

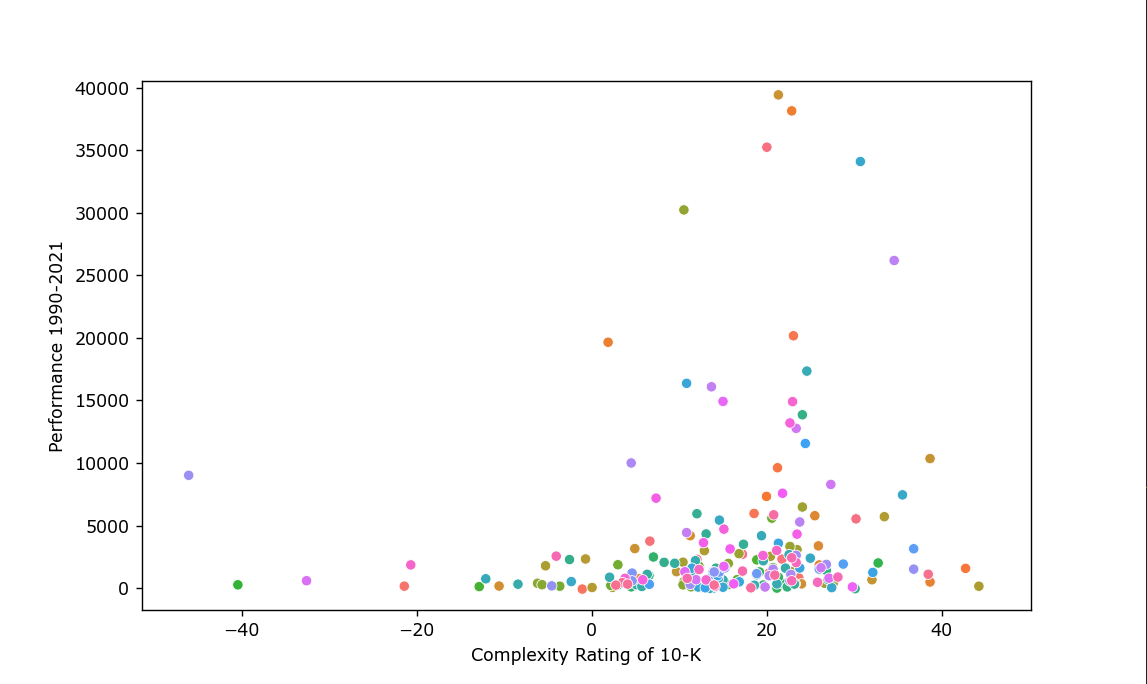

Testing the historical performance of company's stocks based on the inherent complexity of their 10-K report filed with the SEC.

The "complexity" score of each report was determined by a Flesch-Kincaid readability scoring system.

Overview of Python scripts used for analysis:

reportCollector.py - Used to gather 10-K filings for each company

complexityAnalysis.py - Used to calculate complexity score of each company based on their 10-K

performanceBacktest.py - Used to calculate historical stock performance of each company

dataAndCorrelation.py - Used to combine the two sets of data into a single file, and to calculate statistical correlation between the two variables

plotData.py - Used to create graph for the resulting set of combined data (shown below)